What Else is Changing in the 2026/27 Tax Year?

It can be hard to keep track of tax changes, with the start of a new tax year often bringing new rates, allowances and other legislative changes. To make things easier, here is a list of the key tax changes that will take effect from April 2026.

INCOME TAX

In 2026/27 income tax rates, thresholds and bands generally remain at their 2025/26 levels. One key change from 6 April 2026 is the rate of income tax that applies to dividend income. For dividends falling within a taxpayer’s £37,700 basic rate band, the rate increases to 10.75% (from 8.75%). For dividends in the higher rate band (£37,701 - £125,140), the rate increases to 35.75% (from 33.75%). The rate of income tax on dividends above the additional rate threshold (£125,140) remains unchanged at 39.35%.

CORPORATION TAX

The rate of tax (known as the ‘s455’ tax charge) on loans to ‘participators’ (broadly shareholders) in ‘close companies’ (broadly companies controlled by 5 or fewer participators), is set according to the dividend upper rate. This means that the tax charge on loans that remain unpaid 9 months and 1 day after the accounting period end will increase to 35.75% for loans and advances made on or after 6 April 2026.

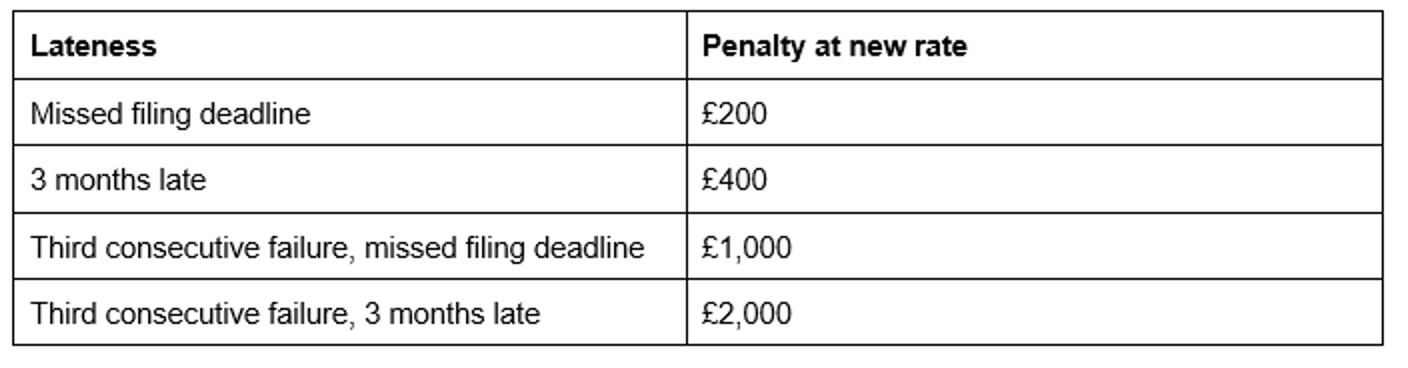

Another key corporation tax change is the new penalty amounts applicable to late-filed corporation tax returns. For returns with a due date that is on or after 1 April 2026, the penalties are:

The CGT rates applicable to gains qualifying for both Business Asset Disposal Relief (BADR) and Investors’ Relief (IR) are set to increase again to 18% on 6 April 2026. The rates previously increased to 14% (from 10%) on 6 April 2025.

VAT

From 1 April 2026, a new relief will exclude most donations of business goods to charities from the deemed-supply VAT rules.